DZ BANK Research – Outlook for 2022

Pent-up demand will boost global economy from summer / inflation will ease over the year – but remain above the ECB target in Germany / DAX to reach 18,000 points

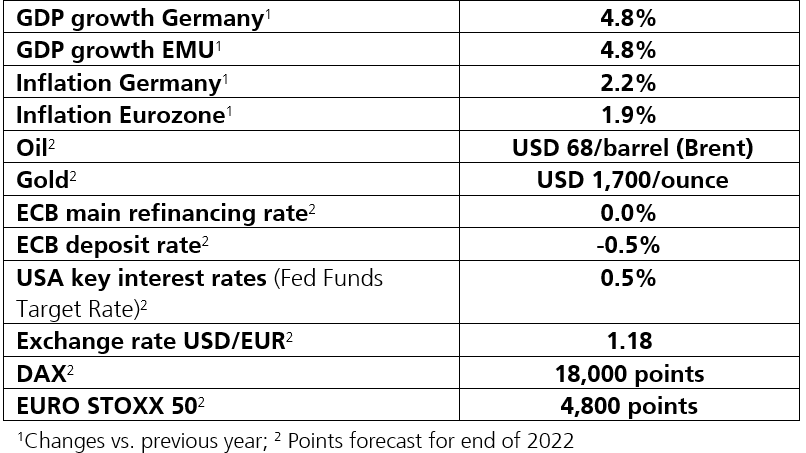

Despite a sharp rise in coronavirus cases and massive supply chain problems, DZ BANK Research views next year with confidence. Our analysts expect a strong economic recovery from the second quarter of 2022, driven by pent-up demand. Increasing vaccination rates will pave the way for a normalisation of everyday life and the economy. The experts forecast global economic growth of 4.4 per cent, with GDP in Germany rising by 4.8 per cent. Continuing low interest rates and a backlog of production orders will propel major share indices to record levels. DZ BANK predicts that the DAX will reach 18,000 points by the end of 2022. Inflation will ease over the year.

The second year of coronavirus was a rollercoaster ride. While global lockdowns had a major impact in the first quarter, the engine of global economic growth started up again everywhere almost simultaneously from April. The German economy grew by 9.9 per cent year-on-year in the second quarter and the Euro area economy by 14.2 per cent. However, demand for energy and intermediate products quickly drove inflation up sharply, causing supply chain bottlenecks. Because many companies were no longer able to fulfil orders, growth declined. Global supply chain problems will continue to weigh on the economy for several more months, only easing from the second quarter of next year.

For the first time since 1990, the US inflation rate reached 6.2 per cent in October. Contributory factors are high energy costs, price hikes for leisure services and expensive used cars. According to the DZ BANK economists, these are extraordinary factors which will have less impact in 2022. Inflation will fall to 3 per cent next year. Since the US health authorities have also approved the coronavirus vaccine for children, and broad sections of the population will receive booster vaccinations, the immunisation campaign should continue to gain momentum. This will also shore up consumer confidence and should curb the pandemic further. The US economy will therefore grow by 4 per cent compared to the previous year.

DZ BANK Research forecasts growth of 4.8 per cent for the Euro area. Supply chains are likely to function more efficiently from the second quarter as the backlog in many ports is gradually cleared. This will help companies to process orders. However, the economic headwind will initially continue to cast a chill in the winter.

Germany: Winter blues followed by strong growth

The German economy is under major pressure to innovate as a result of climate change and digitalisation, but global demand for its products has held up during the pandemic. The processing of full order books will only start to accelerate again in the spring, when important intermediate products such as microchips become more widely available again. The sharp rise in the number of coronavirus cases and the sluggish pace of the vaccination campaign will also be matters of concern for the economy in the coming months. DZ BANK Chief Economist Michael Holstein says that “A general lockdown would be a major disaster and could lead to irreparable damage in the services sector” although he does not expect to see widespread closures again. Analysts are forecasting economic growth of 4.8 per cent.

2.2 per cent: Inflation still above the ECB target

The historic increase in the inflation rate in Germany is mainly attributable to the absence of the “VAT effect” and high energy costs, particularly for oil. Since energy prices will fall again gradually, analysts are predicting an inflation rate of 2.2 per cent for Germany in 2022 – slightly above the ECB target. Nevertheless, there are challenges which could also drive inflation up for longer. Michael Holstein cites here the costly, and still ongoing transformation into a sustained economy and de-globalisation tendencies which are hampering the international movement of goods. Demographic change in the advanced and developing economies could also fuel wages and thus inflation.

Monetary policy: Divided Europe tests central bank mandate

Europe has deployed a monetary bazooka to cushion the impact of the pandemic. Historic support packages are driving debt levels to dizzying heights in many Euro countries. “The role of risk manager has been foisted on the ECB because the Euro area is divided over fiscal policy. Debt levels are not a problem so long as interest rates remain low, but this will change if rates rise sharply. The central bank must also keep a close eye on this because of inflation”, explains Michael Holstein. DZ BANK Research does not nevertheless expect a turnaround in Eurozone interest rates next year. Money will remain cheap, making it even more important for the markets to be well prepared for changes in the medium term.

Traffic light coalition: New government could become bogged down in reforms

The FDP would most likely sound a note of caution on the budget in the new German government, resisting any relaxation of the Maastricht criteria. After initial euphoria, the new three-way government could quickly come unstuck over the setting of important economic policy goals for Germany – for example in relation to housebuilding. “Plans to build 400,000 new housing units in a year could fail due to a shortage of workers and materials” stresses Holstein. In addition to climate change, the pension system in particular poses a major challenge. A flexible retirement age and a state sponsored share fund could help. “This should be started while interest rates are low”, stresses Holstein.

Stock markets: Year of the cyclicals will lead to record earnings

According to Chief Investment Strategist Christian Kahler, the party season in the stock markets will continue beyond the turn of the year. Stock indices in the USA and Europe in particular are likely to run neck-and-neck. Kahler predicts that the DAX will reach an historic 18,000 points: “Delayed does not mean cancelled – if orders can be fulfilled once normal supply chain functioning is restored, this will give cyclicals and German stocks in particular a clear run.” Other European stocks could also benefit. Analysts expect the Euro Stoxx 50 to reach 4,800 points by the end of 2022. In the USA, as well as cyclicals, companies which are not dependent on economic cycles – particularly Big Techs – will deliver strong results. The S&P 500 should climb to 5,200 points over the year. Other top performers – in addition to the tech sector - could be energy companies and banks.

Sample portfolio: USA and Europe dominate

Kahler stresses that ”the biggest risk for investors is not being invested in the stock market in 2022“. This is because of the growth in corporate earnings, stable business models and low interest rates. However, a broad investment spread is still important. Approximately twenty-five per cent of his sample portfolio consists of European corporate bonds. European energy stocks and bank stocks account for 5 per cent each. DAX stocks represent 13 per cent of the portfolio and stocks from the Nasdaq 100, 9 per cent. This year the sample portfolio has gained 5.7 per cent.

Download: Presentation of DZ BANK Research on the 2022 Annual Outlook